Help Articles & FAQ

Who Gets Credit Card Fees, Where they go, Why

(Feel free to comment and post your own questions. Free help & support.)

LETTERS: Q & A

Free Help

Call our Merchant Relations consultants for free help, quotes or analysis of your current merchant statement or for new service at 1-800-545-1995.

Call our Merchant Relations consultants for free help, quotes or analysis of your current merchant statement or for new service at 1-800-545-1995.

ARTICLES:

I can't understand my credit card statement!

Tricks of the trade:

Cancellation Penalties and Early Termination Fees

REFERENCE:

- usa.Visa.com

- MasterCard.us

- DiscoverCard.com

- AmericanExpress.com

- glossary of terms

- PCI compliance

- FDIC.gov

- TransFirst.com

Also Call Us for Cash Advances against future credit card sales!

You may be able to borrow up to ten times your monthly volume with no credit checks.

Rates Vary By Industry Type

RETAIL

face to face vendors

MOTO

mail order or telephone order

ECOMMERCE

all internet based transactions

RESTAURANT

Including quick purchase, small ticket

SUPER MARKET

grocery stores with over 20% perishable

FUEL

gas, propane, incl. pay at pump

HOTEL

motel, lodging with deposit reservations

AUTO RENTAL

advanced deposit on reservations

EMERGING MARKETS

education, charity, government, utilities

Fees Fees Fees Fees Fees...

It seems like there are fees for everything for every kind of reason.

But, where do these fees go?

Who Gets All Those Fees?

how they’re assessed, where they go...

There are many different fees because there really are many costs involved in getting your customer’s money into your bank account. Did you also know that there are over 38 types of Visa cards, 44 types of MasterCards and each have a different rate?

As you can imagine, there is more happening with a transaction than it appears. This is because there are many “gatekeepers” involved in an exchange (transaction).

The only actual exchange is electronic data. When data travels through these gatekeepers, they charge a toll, just like a toll booth.

Just because it all happens within seconds, does not mean it only travels a short distance. On the contrary, a single transaction usually travels thousands of miles, back and forth from coast to coast.

Let’s look at where this data goes

- Your Terminal or Gateway (gateways may be required if you have a POS system, software or website shopping cart).

- Network (speaks a language which must be compatible with your Processor, or requires "Middleware").

- Processor (responsible for the entire transaction, start to finish).

- Acquiring Bank (The Processor's Bank)

- Issuing Bank (the Cardholder’s bank)

- Back to Acquiring Bank and Processor

- Your Business Bank Account

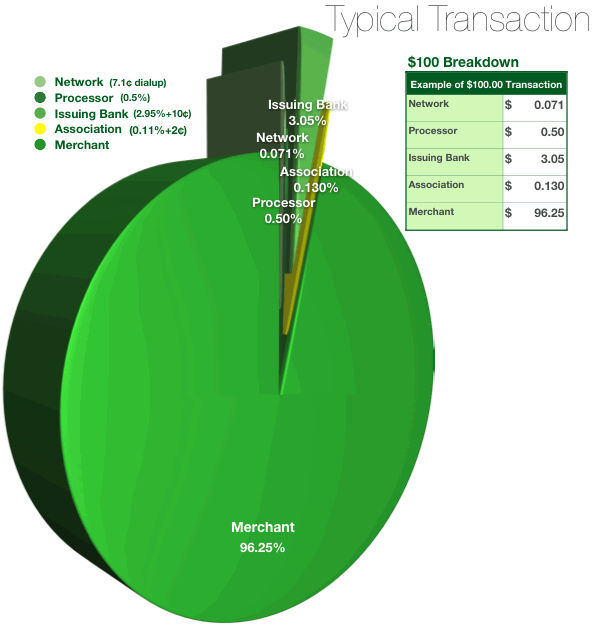

Let’s break down a transaction

Now that you know who is involved, let’s follow the money to see how these fees are distributed.

Let’s assume your customer makes a $100 purchase using a Visa card. Now, you cannot tell which Visa card he gives you, but only Visa knows that it might happen to be one of their business cards called “Commercial Card Electronic.”

In the chart below, here's what happens:

- the bank issuing the cardholder his Visa (Issuer) takes: $3.05 (2.95% + 10¢),

- Processor gets 50¢ (0.5% depending on the merchant's industry & risk),

- Network gets 6.5¢ unless the connection is via internet which is only 4¢),

- Visa Association gets 13¢ (2¢ plus 0.11%).

(Remember that it is the Card's Association who determines how much Issuing Banks get, because they set Interchange rates).

You, the Merchant, would get 96.25% in this case, or $96.25 of your $100 sale.

Your Effective Rate would be 3.75%, if you divide your total fees by the total sale volume. You should do this to your total monthly statement to compare your Processor's rates.