Help Articles & FAQ

Understanding Straight Pass Through Pricing

(Feel free to comment and post your own questions. Free help & support.)

LETTERS: Q & A

Free Help

Call our Merchant Relations consultants for free help, quotes or analysis of your current merchant statement or for new service at 1-800-545-1995.

Call our Merchant Relations consultants for free help, quotes or analysis of your current merchant statement or for new service at 1-800-545-1995.

ARTICLES:

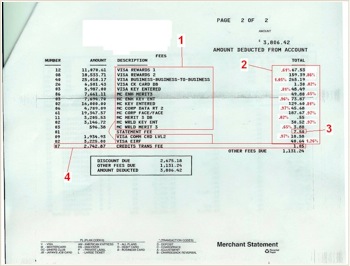

I can't understand my credit card statement!

Tricks of the trade:

Cancellation Penalties and Early Termination Fees

REFERENCE:

- usa.Visa.com

- MasterCard.us

- DiscoverCard.com

- AmericanExpress.com

- glossary of terms

- PCI compliance

- FDIC.gov

- TransFirst.com

Also Call Us for Cash Advances against future credit card sales!

You may be able to borrow up to ten times your monthly volume with no credit checks.

Rates Vary By Industry Type

RETAIL

face to face vendors

MOTO

mail order or telephone order

ECOMMERCE

all internet based transactions

RESTAURANT

Including quick purchase, small ticket

SUPER MARKET

grocery stores with over 20% perishable

FUEL

gas, propane, incl. pay at pump

HOTEL

motel, lodging with deposit reservations

AUTO RENTAL

advanced deposit on reservations

EMERGING MARKETS

education, charity, government, utilities

Understanding your statement should not require an MBA from Harvard. The first thing to understand about fees is where they go precisely.

Stop inflated, padded fees

straight pass thru means true cost

Straight Pass Through is a term applying only to a Merchant Account with Gross Billing or Interchange Plus, whose surcharges are passed through at cost, i.e.: no markup.

Each Card Association (Visa, MC, Discover or Amex) has many different individual designations of their cards, respectively. For example, there are 38 varieties of Visa, 44 varieties of MasterCard, and so forth.

When you accept a credit card from a customer, you have NO idea which type of Visa or MasterCard it is. They all have 16 digits, 4 digit expiration, and 3 digit CVV2 code.

Card Associations surcharge for:

- rewards cards

- travel/entertainment cards

- international/foreign cards

- preferred cards (no credit limit)

- commercial cards

- business cards

- corporate cards

- commercial electronic

- purchasing cards

- and many more!

It All Comes Down to Risk (supposedly)

On each of their cards, the Card Associations assess the risk of disputes, chargebacks and incidence of fraud of their individual card types.

They charge MORE when they assess higher risk. For example, oftentimes business cards get abused, stolen and employers commonly dispute transactions. So as you might expect, business cards often have the highest surcharges.

Debit Cards Are Best

Because Debit cards have a decreased risk of fraud, Issuing Banks give a Rebate of about 0.5% on all debit cards. Not only do many Processors keep this rebate without passing it on to Merchants, some actually charge MORE for it!

Interchange

The list of these Surcharges on all their card types is called Interchange and can be found on our glossary page here.

Double Dipping

Sadly, a lot of Processors pad the surcharges for additional profit. They’re not content making a profit solely on the Discount Rate (base rate usually on the front page of Statement). So they double dip by jacking up the rates on surcharged cards.

Tiered Billing

Sometimes surcharged cards are referred to as MidQual or NonQual on Tiered billing statement charges because they do not qualify at the base rate (Discount Rate).

There are other surcharges incurred as well under certain circumstances:

- key entered where card not present (CNP)

- transaction did not settle (batch) within 24 hours

- address verification failure

- sales tax code ignored

- verification prompts ignored

If you are on Tiered billing, see Tricks of the Trade: Tier Billing